Deep Dive: Micron Earnings; Korean Debt Unwinding; Leverage Rebalancing

Why Microns earnings will lead to an asymmetric bull rally.

Micron’s Earnings:

Micron ($MU) just printed a massive earnings beat across the board, soaring past every single estimate…

Revenue: $41.46 billion versus $23.86 billion for the prior quarter and $9.30 billion for the same period last year; roughly +346% YoY and +74% sequentially

Non-GAAP EPS: $25.11; GAAP EPS $24.67 (GAAP net income of $28.24 billion, non-GAAP net income $28.86B)

vs. consensus of roughly EPS of $20.39 and revenue of $35.1 billion; so a ~$6B revenue beat and a $4.50+ EPS beat

Board of Directors declared a quarterly dividend of $0.15 per share; ended the quarter with cash, marketable investments, and restricted cash of $30.2 billion

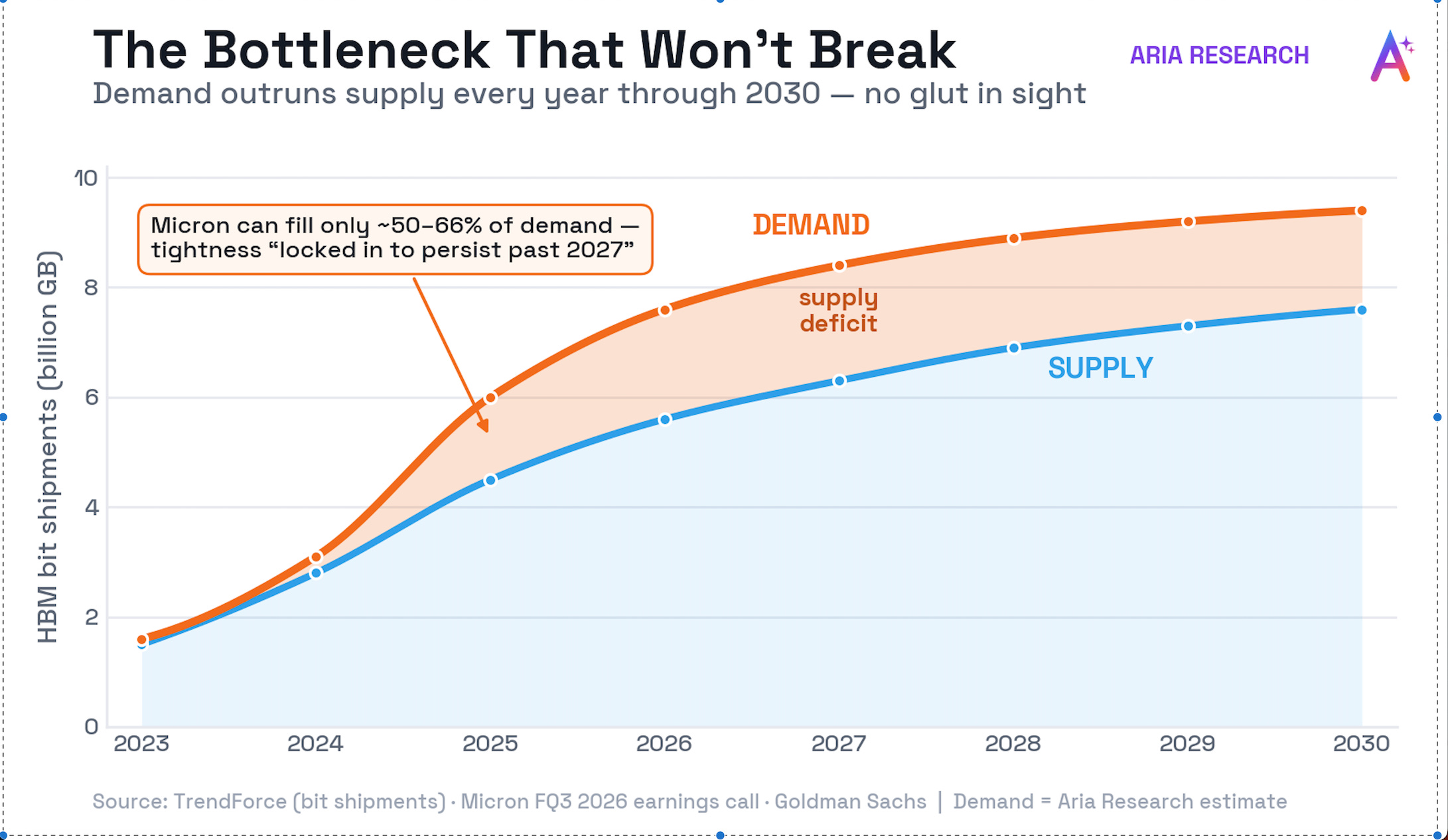

On top of those numbers, Micron increased their margin from 81% - 86% QoQ. This is a company who is printing cash, and those insane margins prove demand is insatiable, and that they have all the pricing power in the world. This earnings call wasn’t just pivotal for Micron as a business, it was a necessity for the AI boom to keep going strong. You see, Micron is one of the global leaders in HBM-manufacturing. HBM is one of the most important bottlenecks in the entire AI stack, and as agentic AI makes its way to the enterprise/consumer level, the need for HBM will only increase. If Micron showed a slowdown in HBM demand, or the beginning telltale signs of an “oversupply,’’ Micron would’ve crashed, and brought the entire market down with it. Micron actually printed the opposite. CEO Sanjay stated that they foresee the HBM bottleneck persisting well past 2027, as well as their pricing power. If you read our previous 2 memos, you would’ve been caught up to speed with this idea. One of our lead AI/Semi analysts, on YouTube and X, has been calling for the HBM bottleneck to persist into 2028 since early April. Once again, this earnings call reiterates this thesis…

Seoul, South Korea:

One of the most random drops we saw in the markets occurred on June 23rd, caused by Korean Debt/leverage. We made a memo regarding the severity of the “leverage issue” sneaking up on Korean investors; primarily retail investors, who have been taking out record amounts of debt in order to invest into tech-heavy companies. Most of these investments being Sk Hynix and Samsung, who make up 42% of the KOSPI index.

Due to the very weak Korean currency (Won), The bank of Korea is planning on raising interest rates toward 3% by September, in order to strengthen it. Seoul, South Korea has already “launched its first joint FX-bank inspection in 14 years, tripled its FX-stabilization bond ceiling, and put the pension fund into $54B of dollar-forward hedging. Tighter Korean policy is contractionary, so the weak won converts straight into the same "rate hike" pressure that's causing de-risking in the leveraged AI trade.”

The MSCI, once again, had excluded Korea from its developed market watchlist, removing the passive-inflow catalyst foreign investors had bought in anticipation of. (About $2.5 billion of foreign capital fled in a single session)

When you have a vast amount of equities being funded by debt, downturns can turn into full on crashes. When and investor borrows money to pay for an investment, the collateral put up is the shares themselves; and when the collateral is losing value, often times, investors cut their losses so they can maintain solvency and pay off their debt. Coupling this with the MSCI exclusion, rate-hikes, and over-leveraging, you have a recipe for a potential market crash. And that’s exactly what happened… for the most part. Leveraged positions like the 2x Sk Hynix and Samsung ETFs both were forced to continuously sell into the close to maintain their multiplier rates. This amplified the sell-off, leading to more and more debt unwinding.