ALERT: Why Markets Crashed Today

Explaining the root causes, and what it means for your stocks.

If you wanted some red light therapy, you probably decided not to go to your local spa; instead, you looked at CNBC. At the time of writing this article, the Nasdaq 100 is down 2.88%, and the S&P 500 is down 1.30%. Leveraged ETFs like the Direxion 3X Bull Semiconductor ETF are down 21.98%. Overall, not a great day for investing.

You and I alike probably woke up today asking ourselves, “Why are all my positions getting killed?” No need to look any further, because Aria has the answer.

The KOSPI Sell-off

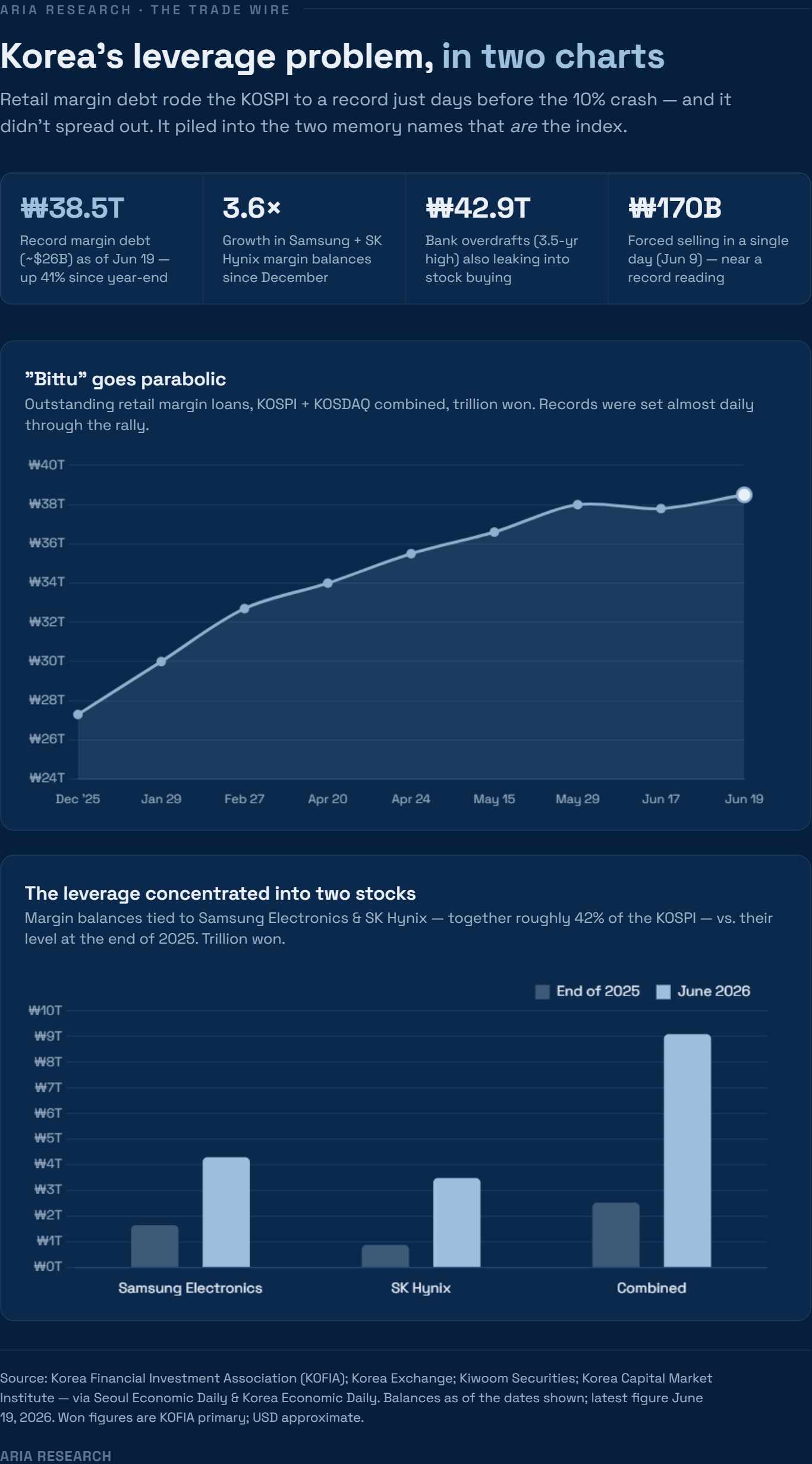

The KOSPI fell 9.99% on June 23rd in an accelerated liquidation. Led by SK Hynix and Samsung (which make up roughly 42% of the index), each dropped around 12% intraday. After a 164% runup during the year, this was the most violent single-session loss of the year. This huge market sell-off was sparked by a few main catalysts that added fuel to the fire.

Investors Are Over-Leveraged

The KOSPI index is the worlds most concentrated expression of the global AI/memory trade, with almost half of the index being SK Hynix and Samsung, the two largest HBM suppliers in the entire world. This in itself isn’t an issue, it only becomes an issue when you take into account how this trade is being funded. Koreans are taking on large amounts of debt to fund their invesments. Korean margin debt hit a record high in June 2026, with specific “leveraged products” being tied directly to the AI/Chip sector. A 3% drop in the overall market could represent a 10% drop in a “debt leveraged” trade; coupling that with high beta AI/Chip companies prone to vast fluctuations, can lead to margin calls at a rapid scale. Margin balances in SK Hynix and Samsung rose from 2.53T won by the end of 2025 to 9.10T won by June 17 2026; roughly 3.6x in 6 months. The collateral put up in these trades are the shares themsevles, so when price falls, the collateral can fall short, leading to margin calls and forced selling of the shares. This already happened recently, with forced sales topping 100B won for five straight sessions (june 5-9), with 169.8B won liquidated on June 9th alone.

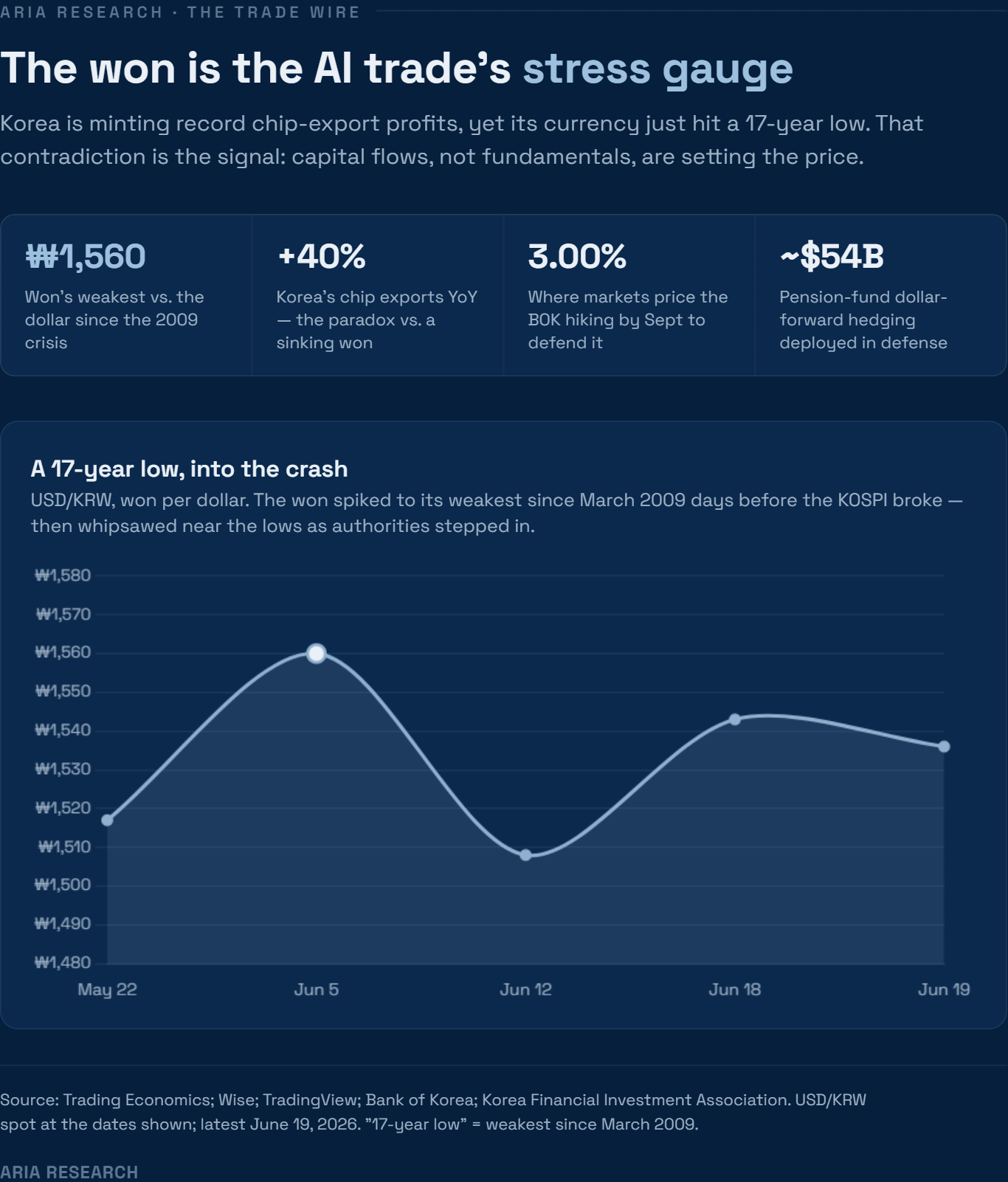

The Weak Korean Currency

Coupling over-leveraged margin calls with a depreaciating won, and you have a recipe for an accelerated sell-off. The won currently sits a 1,533 per US dollar; its weakest since the 2009 financial crisis. In order to combat this, the Bank of Korea is planning on raising interest rates toward 3% by September. Seoul has already launched its first joint FX-bank inspection in 14 years, tripled its FX-stabilization bond ceiling, and put the pension fund into $54B of dollar-forward hedging. Tighter Korean policy is contractionary, so the weak won converts straight into the same "rate hike" pressure that's causing de-risking in the leveraged AI trade. When rates rise, the cost of debt does as well, so when this happens, the last thing you need as a leveraged investor is your collateral losing its value. If this does occur, you will be forced by the lendor to liquidate your position.

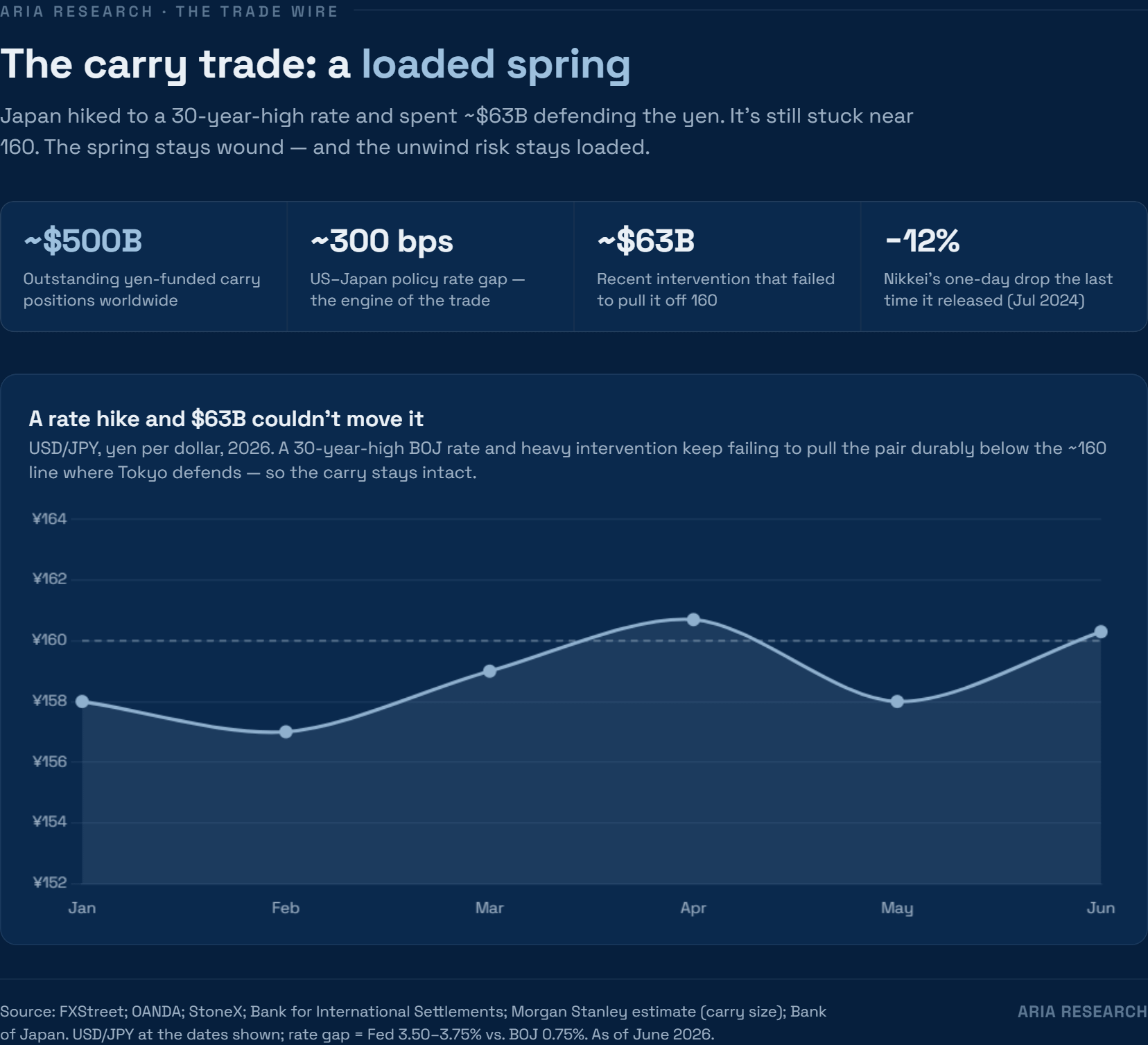

The Japanese Carry Trade

On top of everything we have discussed, the loaded spring of the Japanese carry trade could release at any given moment. Like Korea, the Bank of Japan is seeing the weakest yen in over 4 decades. Because of this, inflation is running rampid in Japan. This forces the hand of the BOJ to raise interest rates to protect against the inflation issue and strengthen their currency. As we know, the Japanese carry trade has been funding Mega-Cap AI companies in the United States for many years. Insitutions would use this as an “arbitrage technique.” They would borrow yen at an extremely low interest rate, convert it into USD, and purchase treasuries and or stocks that yeild higher returns than the interest they owe.

Looking at the chart above, there is roughly $500b in outstanding yen-funded carry positions worldwide, the majority of which are US equity-related. When rates are rising in Japan, this forces those institutions to adjust their risk. Often times by liquidating the high-beta tech names in order to prevent themselves from being “margin-called.”