Power Becoming The Product: The Interconnectivity Bottleneck

How the constraint on AI data centers has moved from inside the rack to the grid outside it. The timelines, the four stacked queues, whether it becomes a hard ceiling, and who actually wins.

The Context

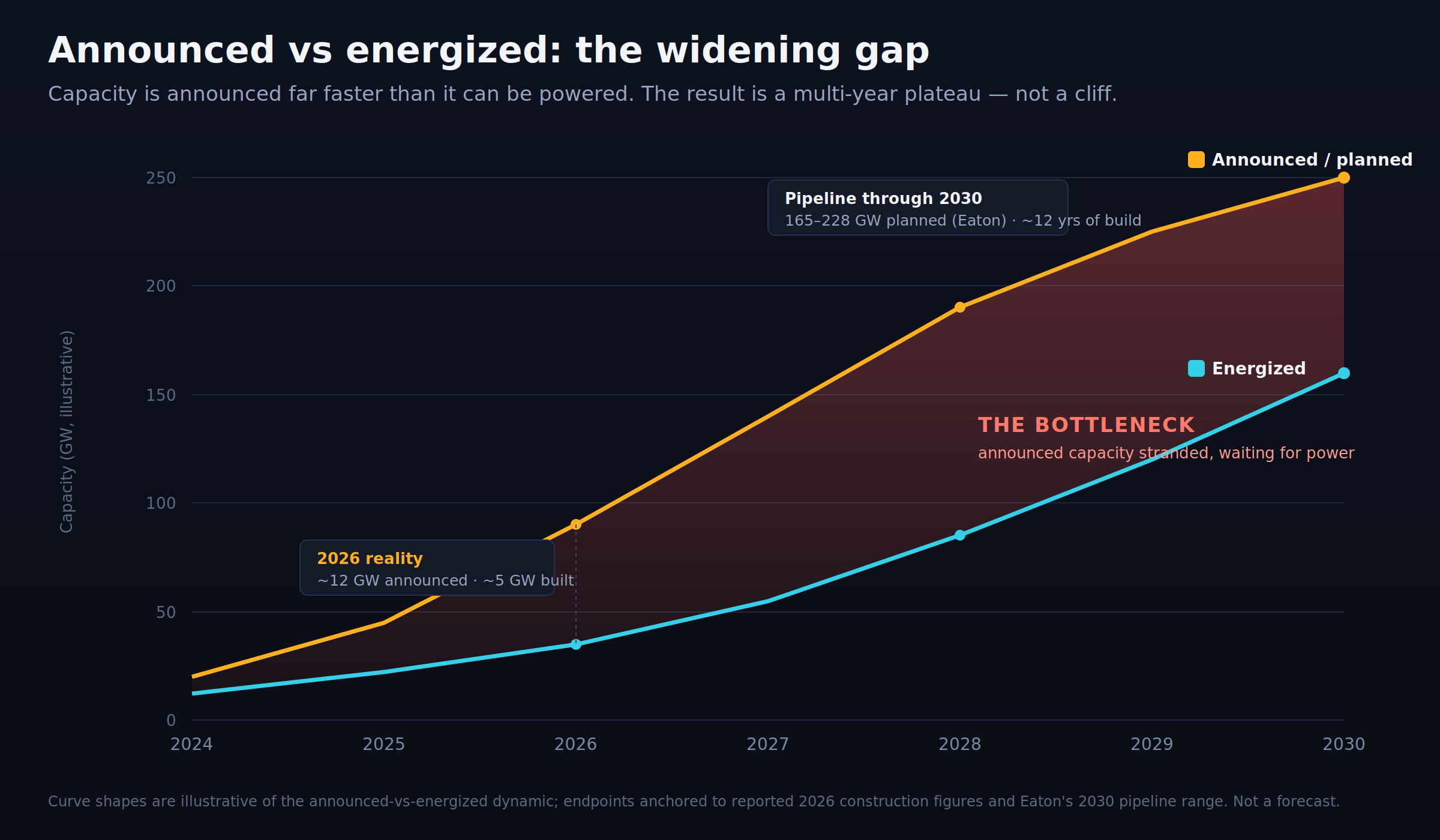

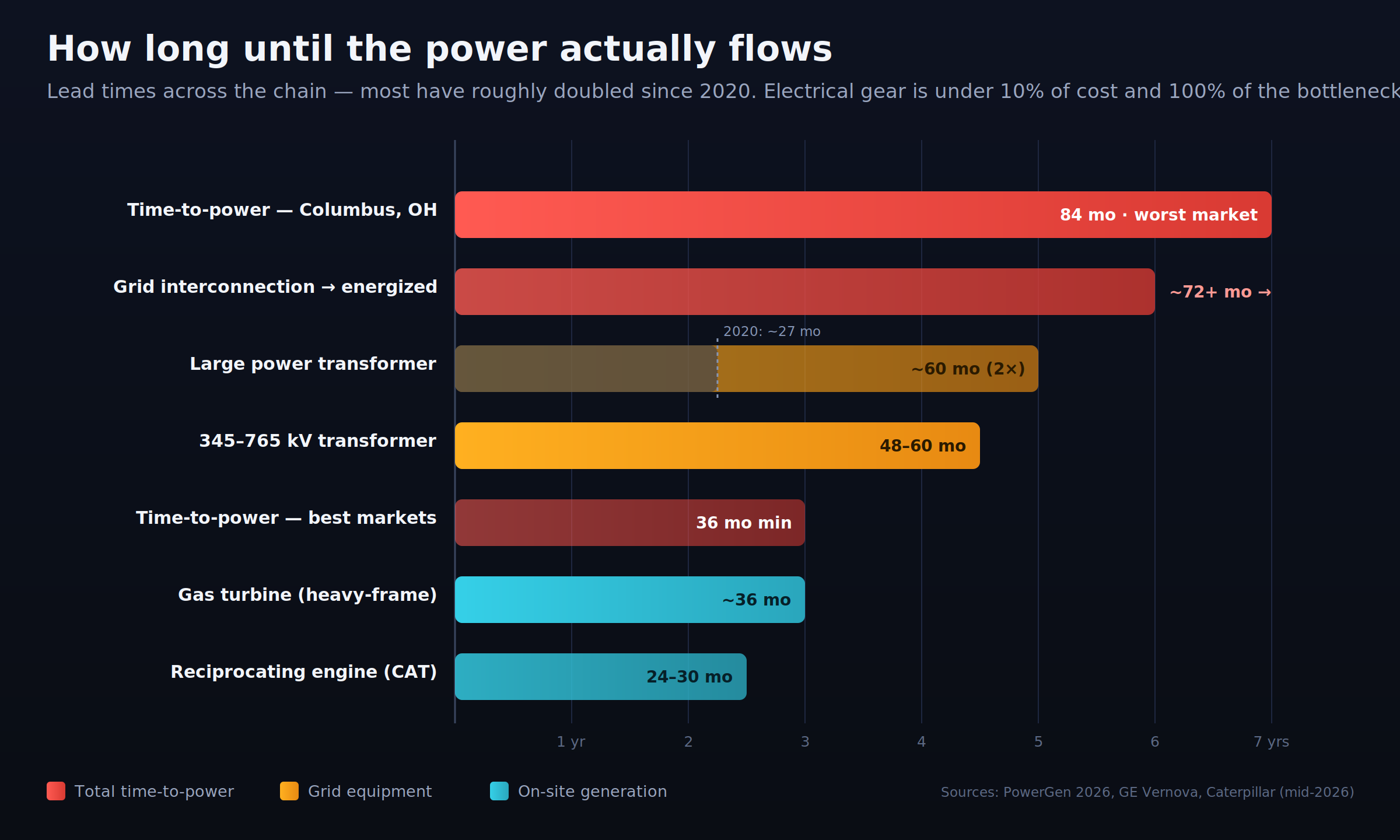

Nvidia is shipping. That is no longer the constraint. A finished rack such as the state-of-the-art 800V Vera Rubin or Rubin Ultra rack is just an expensive piece of parts until it is energized, and getting energized now runs through a chain of multi-year queues that the chip cycle has badly outrun. The single most quotable data point in the whole debate captures it: of the roughly 12 GW of 2026 U.S. data center capacity announced across about 140 projects, only ~5 GW is actually under construction, with the rest stuck in the “announced” stage despite normal build times of 12–18 months. Electrical equipment is under 10% of total data center cost and 100% of the bottleneck.

This report is about that bottleneck: what it actually consists of, how long each piece takes, whether it becomes a true ceiling on AI scaling, and which companies are positioned to profit from relieving it. The short answer on winners: the money is moving away from the chip and toward the grid-infrastructure layer. Transmission builders, transformer and switchgear makers, and on-site power generators, because that is where the scarcity now lives.

The Interconnection Bottleneck Deep Dive

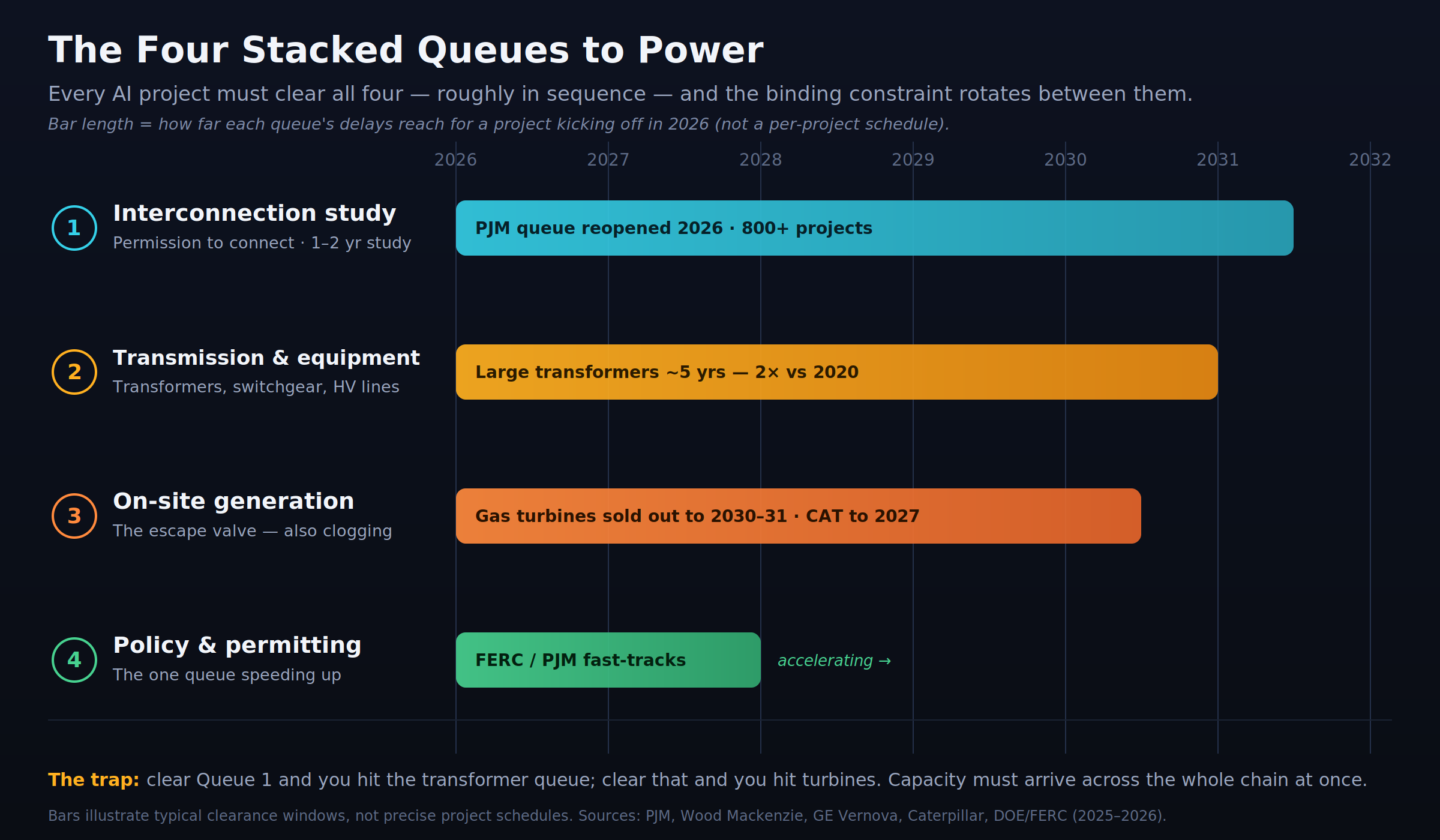

The cleanest way to understand why this is so intractable is to see that it isn't one queue: it's four distinct queues stacked on top of each other, each with its own multi-year clock. A project has to clear all four, roughly in sequence, and the binding constraint rotates between them.

Queue 1 — The interconnection study (permission to connect)

This is the grid operator’s process for studying and approving a new connection. In PJM who is the regional operator covering the Mid-Atlantic and the epicenter of the data center surge became so clogged that PJM effectively froze its queue in 2022 to rebuild the entire process, only reopening it in April 2026 with more than 800 projects in progress. PJM has since pushed over 170,000 MW of generation requests through study and is clearing the last ~46 GW of its transition backlog by the end of 2026.

The reformed “Cycle” process promises one-to-two-year study reviews. But two facts gut the apparent improvement:

A signed interconnection agreement is the midpoint, not the finish. After the agreement comes permitting, financing, equipment procurement, and construction. Realistic commercial-operation dates for projects entering the 2026 cycle stretch into the early 2030s.

The demand wave keeps outrunning the throughput. PJM expects 30+ GW of new demand between 2024 and 2030, driven largely by data centers. Wood Mackenzie pegs PJM-utility large-load forecasts at ~55 GW by 2030 and ~100 GW by 2037. Some of that is “phantom load” (developers filing the same project across multiple utility queues to hedge their bets) which inflates apparent demand and clogs studies further.

The scale mismatch is structural: utilities designed interconnection processes for 50–100 MW industrial loads. In roughly 15 months, typical hyperscale project size jumped from 100–300 MW to 1 GW or more projects that rival baseload power plants. The planning cycle simply was not built for it.

Queue 2 — Transmission and grid equipment (the physical hardware)

Permission is useless without the tools to move the power. This is where lead times have blown out the most:

Large power transformers that were able to be obtained 24–30 months before 2020 now stretch toward five years. The big 345kV–765kV transmission-class units run four to five years as well.

Switchgear is similarly constrained.

These are globally supply-limited, hard-to-scale factories, and data centers are competing for the same units utilities need for ordinary grid maintenance and replacement.

The transmission build itself including high-voltage lines, substations, and load centers are a specialized construction problem gated by skilled-labor scarcity (linemen and electricians) as much as by materials.

Queue 3 — On-site generation (the main escape, which is also clogging)

Because the grid is slow, developers increasingly bypass it by building dedicated power on-site. But this escape valve is filling up too:

Gas turbines: GE Vernova’s heavy-duty turbines are effectively sold out through 2030–2031, with lead times around three years. Its combined backlog has blown past 100 GW and is heading toward ~110 GW against only ~10 GW of annual production capacity which is roughly a decade of output with about a fifth tied explicitly to data-center load. Turbine prices are tracking toward roughly triple 2019 levels (~$600/kW by end-2027).

Reciprocating engines: Caterpillar’s backlog now extends 24 months minimum and is sold out through 2027 even with a major new facility doubling capacity in early 2026; orders placed in early 2026 won’t deliver until 2028, erasing the historical speed advantage of reciprocating engines over turbines. Cummins and INNIO face similar constraints.

The headline number from the field: at PowerGen 2026, one utility planner cited an 84-month (seven-year) lead time to power in a market like Columbus, Ohio, with even the best markets (Pittsburgh, Chicago, Houston, Dallas) requiring 36 months minimum.

Queue 4 — Policy and permitting (the one piece speeding up)

This is the only queue actively improving, under intense political pressure:

The DOE directed FERC to issue rules accelerating large-load interconnection (FERC historically didn’t even assert jurisdiction over load connections), with action targeted for spring 2026.

PJM is rolling out an Expedited Interconnection Track for large advanced projects (250 MW+, capped at ~10 per year), a Reliability Resource Initiative (~8 GW across 41 projects), and a “Bring Your Own Generation” fast track.

The flip side is a hardening political consensus that data centers should pay their own way. The White House and all 13 PJM-state governors jointly insisted in early 2026 that data centers bear the cost of their own load growth rather than shifting it onto ordinary ratepayers (echoed by a federal “Ratepayer Protection” framing). And “connect-and-manage” rules increasingly require large loads to accept curtailment (being cut off during grid stress and falling back to on-site backup) as the price of faster connection.

Will this create a point of complete inability to scale?

The scariest outcome would be a point of such saturation that data center growth is forced to grind to a halt as they just simply cannot bring the power to the facility. Limiting growth by so much causing a huge market freefall as most of these companies are propped up on future revenue forecasts.

In good news, all these queues are rate limiting factors, not complete walls to progress. The US has enough aggregate capacity for approved projects it is just the physical hardware (transmission, transformers, switchgear, turbines and the throughput to connect and deliver said power)

None of these are going to be permanently scarce, its just that each of these in itself is a 3-7 year project. So relief along the supply chain is going to arrive slowly but it is expanding as all these manufacturers are pouring billions to maximize capacity as soon as possible.

The realistic outcome is a plateau, not a full stop. Expect a sustained, multi-year period of roughly 2026 through ~2029-2030 where announced AI capacity dramatically exceeds energized capacity, timelines will slip routinely, power is the explicit gating line item in every site decision, and secured firm power becomes a genuine competitive moat. Buildout continues, but at the pace the slowest link allows. This is why when looking at certain company revenue estimates you can see through 2028 most analysts expect lower growth annually as this bottleneck is well understood and accounted for. (For the most part)

Where a true ceiling can occur. Specific regions like PJM's Mid-Atlantic above all, Northern Virginia, parts of Texas can hit effective saturation where no meaningful new large load can be energized for years. That redirects buildout geographically (toward grid headroom, stranded gas, hydro, or wherever firm power exists) rather than stopping it nationally. The constraint reshapes the map of the AI buildout more than it caps the total.