Micron (MU) Earnings Preview and What to expect from it

A brief preview into Microns upcoming earnings report

The entire market is eagerly anticipating the quarterly earnings report of Micron which will be reported after the bell tomorrow. After such a violent fall in tech stocks today but more specifically memory stocks following the Korean Market implosion there is a very high level of fear and it seems like everyone has an opinion on what will happen tomorrow.

From claims that Microns earnings will absolutely destroy the entire AI/tech super cycle and lead us into a grave recession to Micron having the best report ever and causing a pump in the market never before seen. Traders are taking very extreme stances on this earnings report.

What we are going to do is cut through the noise and tell you everything you need to know regarding Microns earnings report tomorrow.

Market Expectations

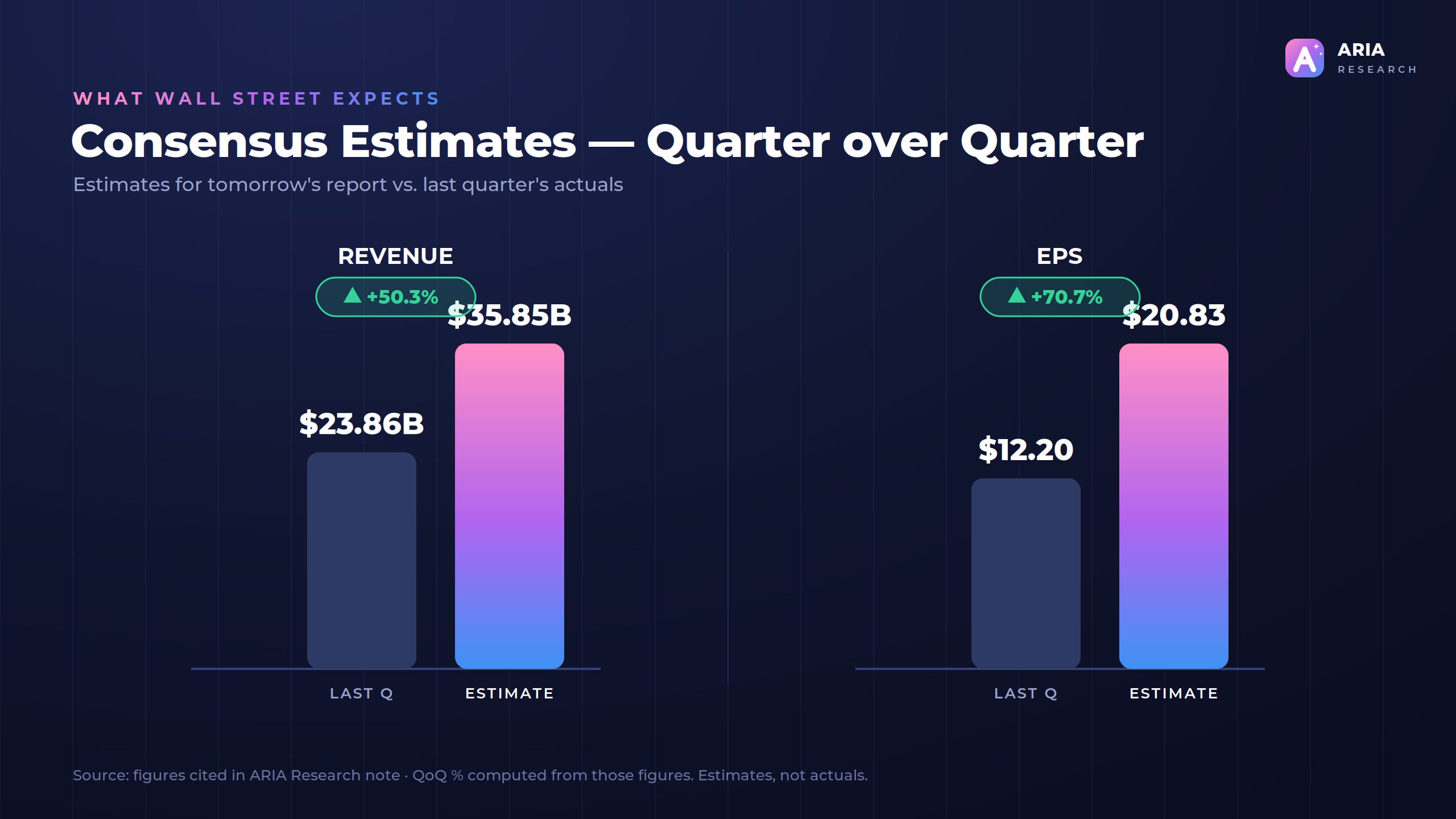

Wall Street is expecting Micron to report revenues of $35.85 billion compared to the $23.86 billion Micron raked in last quarter representing a 50.25% quarterly increase and an EPS estimate of 20.83 vs the reported 12.20 last quarter representing a 70.74% increase from last quarter.

Its clear Wall Street is expecting a huge increase in Microns revenues and EPS and at first glance it can seem like it’s an extreme ask. But once you deep dive into Microns true earning potential it’s clear they will very likely report numbers close to or above these projections.

Now that we know what the market is expecting let’s dive into what our research is telling us and our personal opinions on what the outcome of tomorrows earnings call could be based on our research…

Our Deep Insights into Microns Earnings and Future

We have made it to a point in the AI super cycle where it is clear that memory has become a huge bottleneck. With massive demand and very limited supply that is the core reason behind all of the big memory companies massively increased revenues and EPS.

This bottleneck has given these memory companies all of the negotiating power as they are the ones selling the core piece behind all of the AI hyperscalers ambitions and growth potential. Either they agree to pay whatever memory vendors are charging or they risk falling behind in growth to other companies that will pay that price.

At current estimations we can see this massive pricing power lasting into mid 2027 at the earliest and potentially late 2027 to early 2028 at the latest. However even if supply does increase at that point the prices of DRAM and HBM could and likely will remain elevated from todays prices as demand is unlikely to slow and most likely grow as time goes on.

This will allow all the memory vendors to continue to reach record revenues and earnings for an extended period of time implying a very bullish long term future.

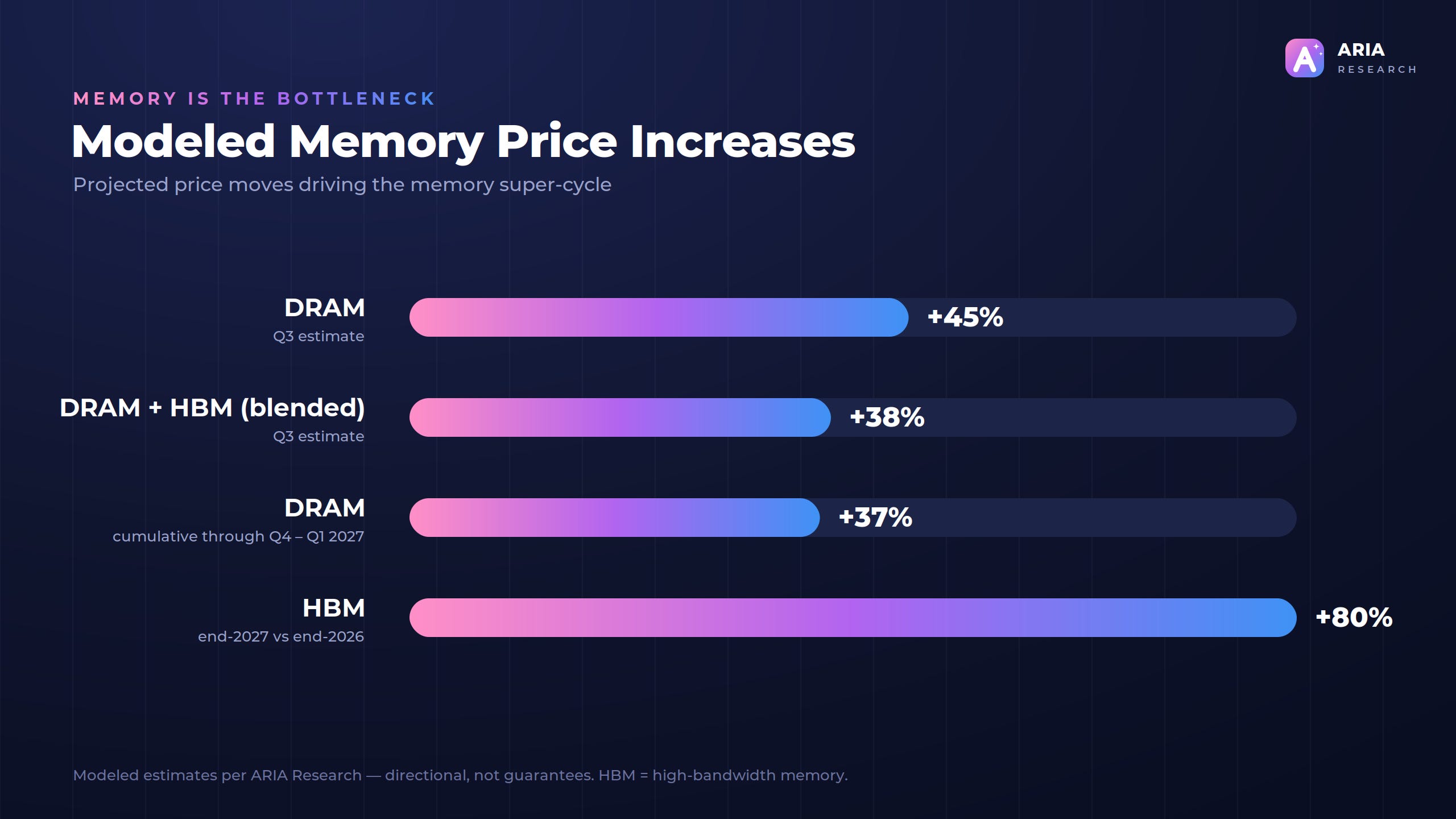

In terms of how much DRAM and HBM are expected to rise; traditional DRAM is estimated to rise ~45% in Q3 with DRAM and HBM combined estimated to rise ~38%. Through Q4 and Q1 2027 DRAM is modelled to rise ~37% total with HBM prices modelled at ~80% increase at the end of 2027 compared to the end of 2026.

All of this is telling you memory is going nowhere soon and will only become a more premium and expensive material in the AI supercycle with the memory vendors continuing to rake in the profits at huge margins.